Climate change-induced flood risk is increasing in the United States. But most don't have insurance

An ABC Owned Television Stations analysis shows millions of properties with substantial risk for flooding by 2053 may not have flood insurance

An ABC Owned Television Stations analysis shows millions of properties with substantial risk for flooding by 2053 may not have flood insurance

As many as 16 million homes and businesses are at major risk of flooding in the next 30 years, and have no flood insurance, according to an ABC Owned Television Stations data analysis.

The analysis, which focuses on how climate change affects flood risk and insurance needs, combines county-level flood modeling data from research/technology group First Street Foundation, and flood insurance policy data from the Federal Emergency Management Agency (FEMA).

FEMA manages nearly all flood policies in the U.S. through the National Flood Insurance Program (NFIP).

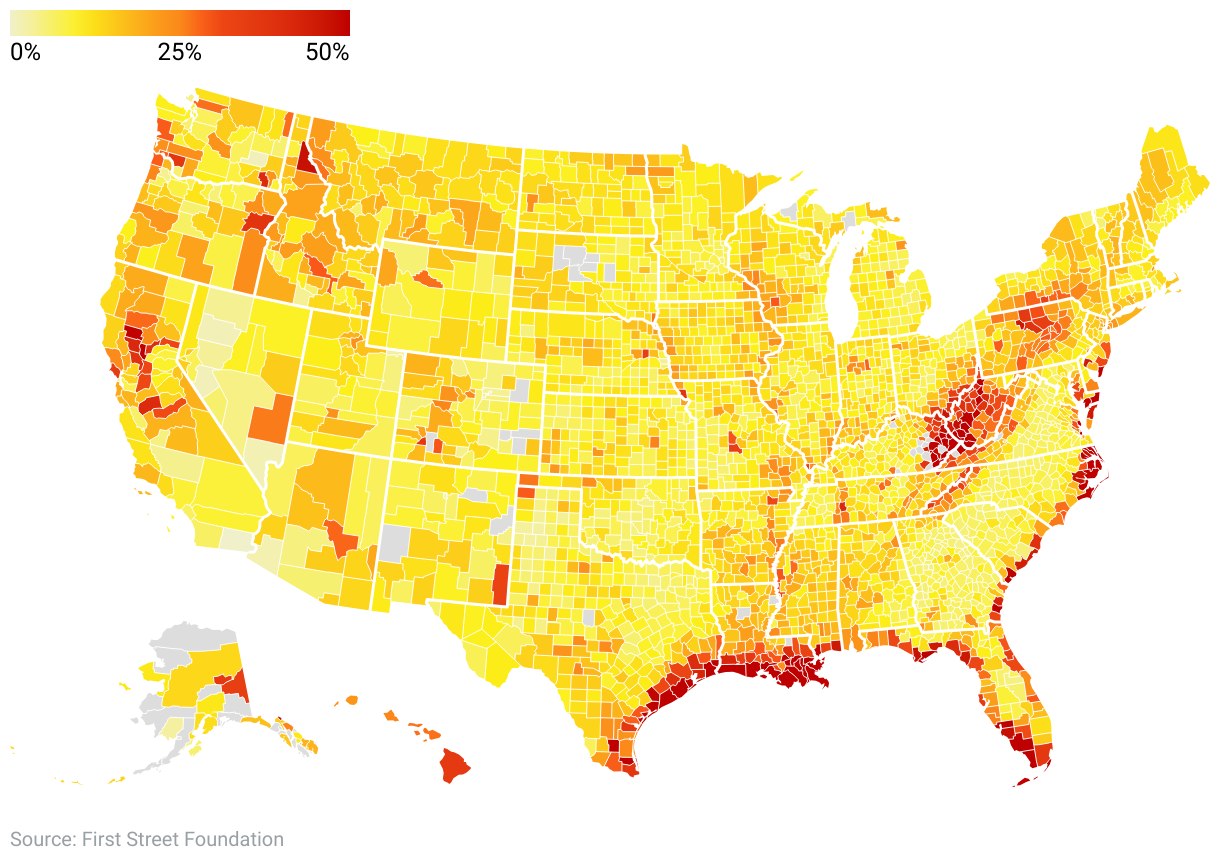

Overall, our analysis of First Street Foundation data identified as many as 20.8 million U.S. properties with an 80% or better chance of flooding by 2053.

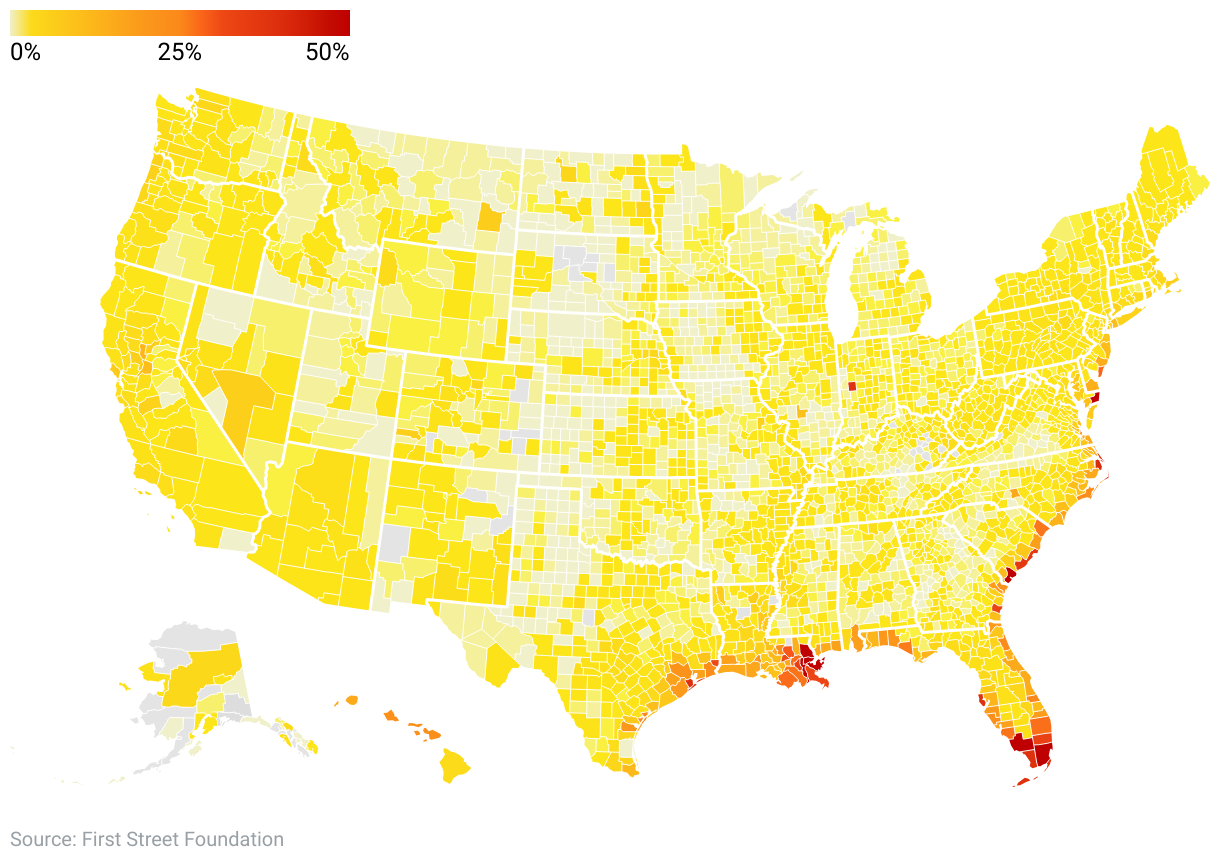

But FEMA county-level data show only 4.7 million flood insurance policies in effect in fiscal year 2022 - creating a gap between property owners facing substantial flood risk and property owners with flood insurance.

The U.S. Congress mandates that financial lenders require flood insurance for properties with a federally backed loan that are located in FEMA-designated Special Flood Hazard Areas (SFHA).

But many of the properties at risk for future flooding in our analysis are not included in those flood hazard zones.

The data show as many as 10.5 million properties with an 80% or better chance for future flooding in counties currently designated by FEMA as "relatively low" or "very low" risk for coastal or river flooding.

With only 1.6 million FEMA-backed insurance policies in those "low-risk" counties, the analysis found that as many as 85% of the properties with substantial flood risk may not be covered.

First Street Foundation researchers say their flood models capture 2.2 times as many properties with significant (a 1-in-100 year or greater) annual flood risk as those in FEMA's comparable flood hazard areas.

By First Street Foundation's count, about 9.8 million of its 17.7 million significant flood risk properties are outside of FEMA flood zones.

As a result, First Street Foundation researchers believe many of those property owners have received no information from FEMA or other government agencies, and may not fully understand - or underestimate - their future flood risk.

The difference in estimates of flood-prone properties evolve from the different approaches taken by FEMA and First Street Foundation to measure flood risk.

First Street Foundation predicts the likelihood of flooding at the property level over a 30-year period - the length of an average mortgage - based on climate change factors and historical events.

FEMA's models rely heavily on historical coastal and river flooding events, and less on surface flooding events from heavy rainfalls in an area, while First Street Foundation models consider environmental factors like precipitation and sea level rise that FEMA models don't include.

Even by federal standards, FEMA's modeled flood maps don't always reflect a true potential for flooding.

One federal report says FEMA's flood maps "vary tremendously" in terms of availability, quality and being outdated.

The report notes that FEMA maps do not consider flood risk from climate change, and cover less than half of America's flood-prone coastlines and only a third of the nation's stream miles. About 22% of the community flood maps are at least 10 years old, and 15% are at least 15 years old.

And like First Street Foundation researchers, consumer advocates believe that many property owners in future high-flood risk areas may be unaware they may even need insurance because their properties are located outside government flood zones.

That would put millions of home and business owners with no flood insurance in danger of paying for water-damaged property, either on their own or through FEMA disaster relief loans.

Restoring flood-damaged homes and businesses with personal finances could be devastating for some Americans.

Federal data show out-of-pocket expenses for flood damage and repairs can be costly -- even for flood policy owners.

On average, flood policyholders still pay about $7,444 on their own, while insurance payouts average about $39,145. About 20% of policyholders end up borrowing money to pay for damages and repairs.

Steep out-of-pocket costs and rising premiums for flood insurance may be forcing some policyholders to reconsider whether they really need coverage.

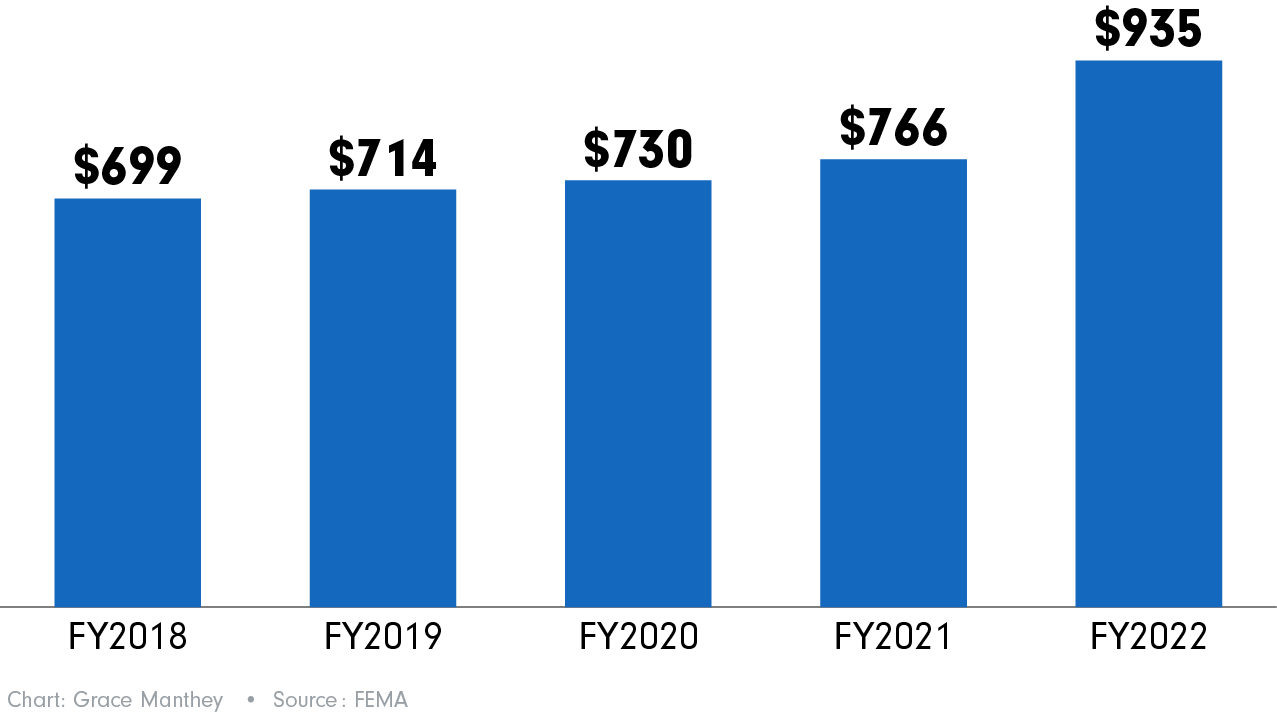

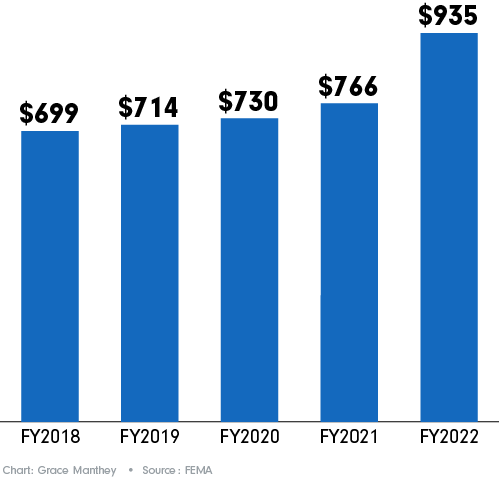

FEMA reports show its average annual flood insurance premium jumped from $699 in FY2018 to $935 by FY2022.

Over the same time, FEMA flood policies dropped from 5,108,000 to 4,719,000.

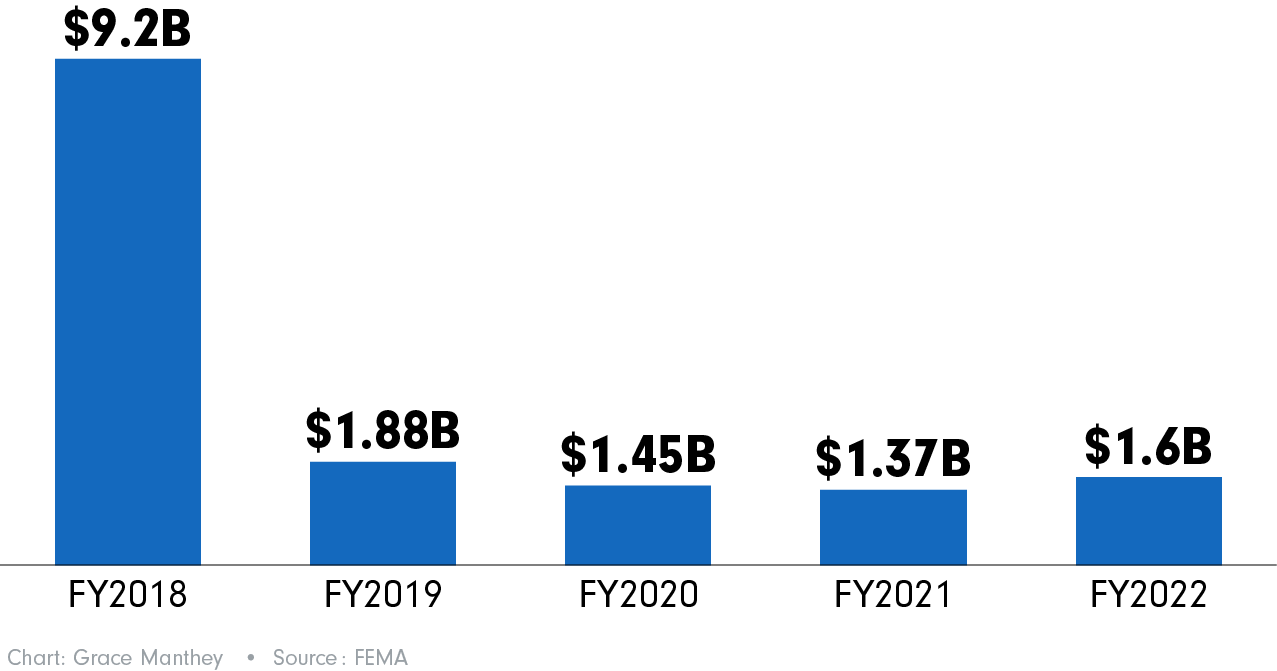

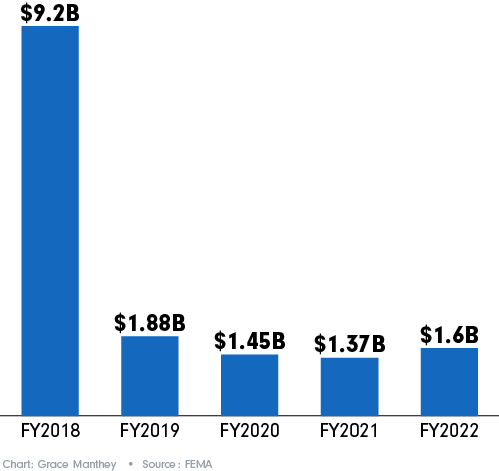

FEMA payouts for flood insurance claims show a rollercoaster ride pattern over those five fiscal years - reflecting various flood events in different parts of the U.S.

FEMA paid flood claims of $9.2 billion in FY2018; $1.88 billion in FY2019; $1.45 billion in FY2020; $1.37 billion in FY2021, and $1.6 billion during FY2022.

While some home and business owners might be on the fence about paying for flood insurance, others in flood-prone areas have been trying to survive without it.

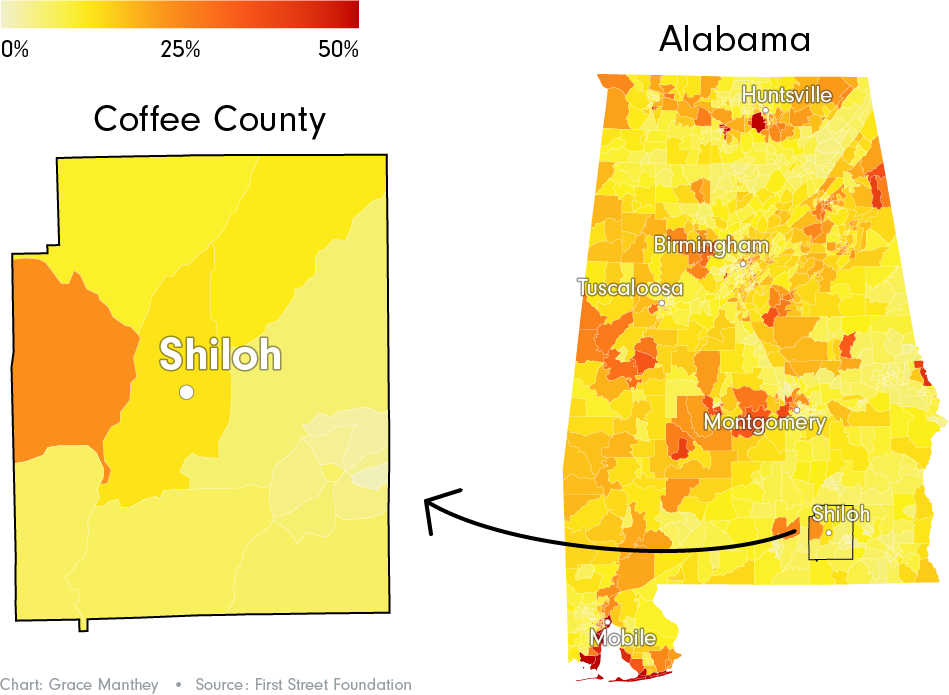

The threat of future flooding already has become a painful reality for residents who have lived for decades in Shiloh, along U.S. Highway 84 in Coffee County, Alabama.

The tiny unincorporated community of mostly-Black residents is in a census tract neighborhood of about 1,700 residents, where median household income is $41,500 - about $27,500 below the national average.

FEMA data show the tract as a "relatively moderate" risk for flooding, and there are no flood hazard zones requiring property owners to have flood insurance.

First Street Foundation models estimate only 13% of the properties in the census tract neighborhood that includes Shiloh are at significant risk for flooding.

But recent environmental and climate changes have now turned Shiloh into a major flood risk.

In 2018, the state widened a stretch of U.S. 84 around Shiloh from two to four lanes, and elevated the highway.

As part of the project, state engineers created a drainage system that allows rainwater runoff from the highway to cascade through pipes and dump into the adjacent lowland residential area.

And since the highway project's completion, it's been raining in droves around Shiloh, creating numerous flooding events.

Data from the National Centers for Environmental Information show Coffee County - and much of southeast Alabama - has reported rainfall totals "above" to "much above" the 57 inches-per-year average for three of the five years since the highway was widened.

Those hefty rainfall totals have translated into an onslaught of flood events in the area.

In fiscal year 2022, FEMA paid out 586 flood loss claims to Coffee County, the sixth-highest total among the 67 Alabama counties. Those claims totaled $17.6 million - the fifth-highest total among Alabama counties.

During a mid-May 2023 event, the Shiloh area experienced at least a foot of rainfall over two consecutive days, and excess water from the highway turned the tiny community into a lake, according to news sources in the area.

"The storms are getting worse," said Timothy Williams, a lifelong Shiloh resident and businessman. "It's not even slowing up. I mean, we never seen it like this.

"If it rains for a whole hour, this whole place is sedated with water."

Williams, who recently opened a restaurant near his home, said floodwaters have already affected the restaurant's septic system.

"We've got a major problem here," he said, referring to the state's altering of the landscape around the highway.

If it rains for a whole hour, this whole place is sedated with water.

"Y'all (the state) are forcin' the water in - on us. It's affecting us, not only physical, mental, but it's affecting our finances. Y'all have flooded us, and we can't even live a normal life."

In a 2022 press statement to a local news station about Shiloh flooding issues, the Alabama Department of Transportation (ALDOT) maintained that its highway storm water system is designed only to move rainwater across the road based on "the natural flow of water across that section of land."

The statement said that water from heavy rainfall moving across the road was coming "from properties on the adjacent side of the roadway (from Shiloh), as it was prior to the construction."

The statement added that ALDOT "continues to evaluate the situation and potential options going forward."

By early 2023, Shiloh residents had had enough.

After repeated calls, they were able to convince representatives from the county, state, and the Federal Highway Administration in Washington D.C., to visit the area and make house-to-house evaluations of flooding conditions.

After that visit, the FHA told residents that it would open a Title VI investigation through the administration's office of civil rights.

But the flooding problems persist.

Y'all have flooded us, and we can't even live a normal life.

Williams and other uninsured neighbors have spent thousands of dollars trying to shore up their homes for the ongoing onslaught of floodwaters.

"We have to come out of our pocket and do different things," Williams said. "Erosions of the drives and water coming over. We have to get out there and dig.

"We've hauled in all this clay, tons of clay, to fix the problem and to try to slope it (water flow). And that didn't work."

While some Shiloh residents said state officials told them they are in a historically flood-prone area, Williams insists residents have never had issues until the highway expansion was completed.

The residents say their insurance companies have never required them to purchase flood insurance.

"We didn't have to have flood insurance because...everything (before the highway project) was flat grounds," Williams said. "I mean, we never had to deal with this...flooding and going on."

Overall, data show only 244 FEMA-backed flood insurance policies in Coffee County in fiscal year 2022 among an estimated 34,000 properties. Coffee County policyholders, on average, pay an annual premium of about $856.

But for uninsured Shiloh residents like Williams, hope lies in the federal civil rights investigation that could correct what they believe is an environmental injustice brought on by Alabama state officials.

"I believe it (the federal investigation) is goin' to lead to something," Williams said. "I believe help is on the way.

"All we're saying here is make us whole. Fix our problem. That's all we're asking."

The ABC OTV analysis found thousands of uninsured property owners in flood-prone communities of color and poorer areas like Shiloh.

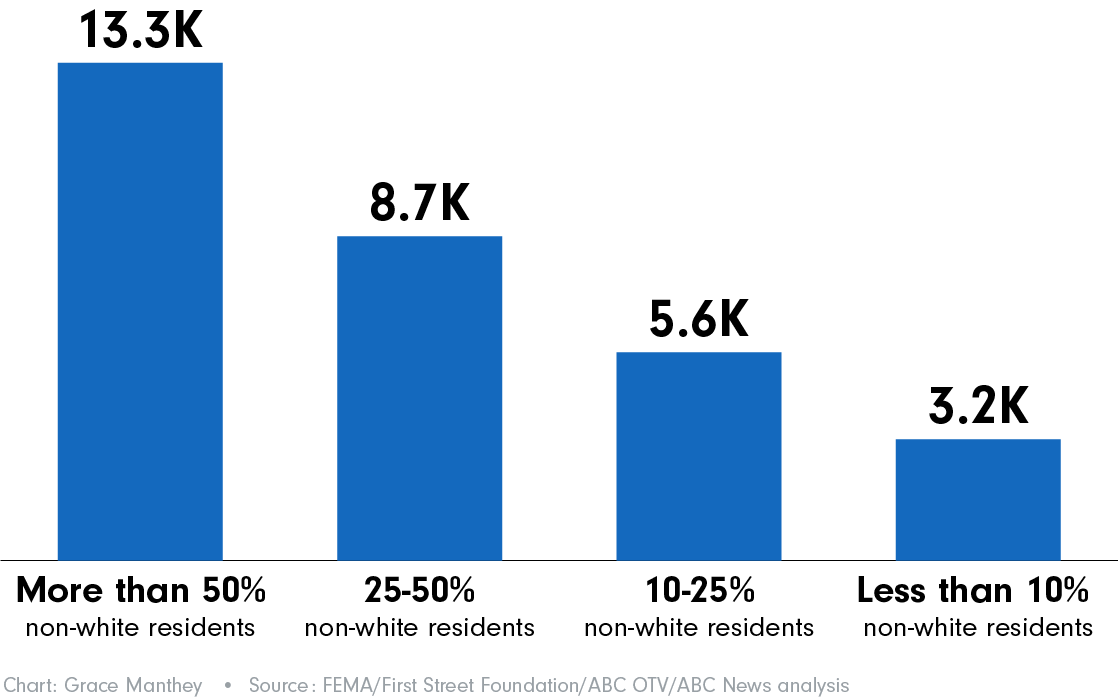

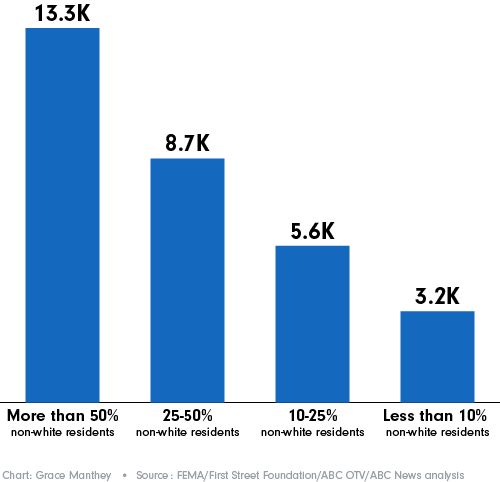

Overall, the data show 396 majority Non-white counties average as many as 8,856 properties with an 80% or better chance at flooding by 2053, and no flood insurance.

By comparison, 961 counties with less than 10% non-White population average as many as 3,135 uninsured properties with that same risk for future flooding.

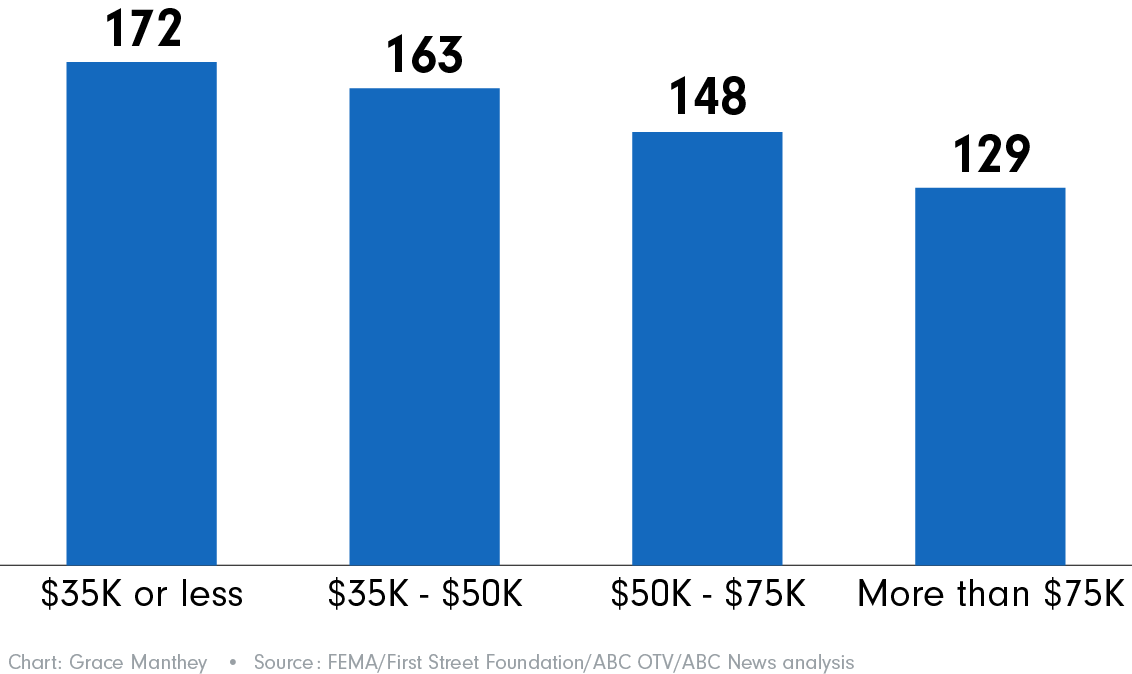

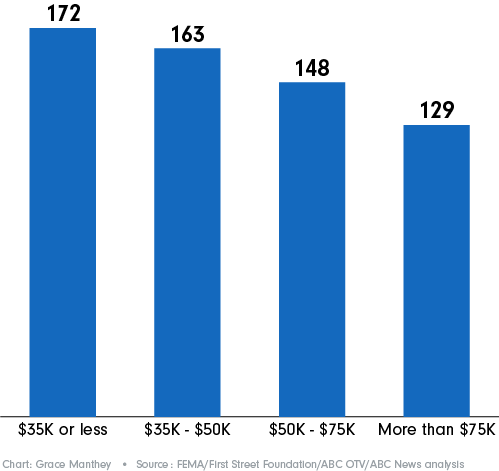

In the nation's 95 poorest counties - where median household income is $35,000 or less — only 5% of the properties with an 80% or better chance of future flooding have flood insurance.

Compare that to the 359 wealthiest counties, with median household income of more than $75,000, where as many as 23% of properties with that substantial flood risk are insured.

The analysis showed extreme examples of properties facing substantial flood risks in Southern counties.

About 10.1 million properties in the South have an 80% or better chance of flooding by 2053, more than twice as many properties as any of the other three census-designated U.S. state regions (Northeast, Midwest and West).

In the 1,442 Southern counties, as many as 6.5 million of those significant flood risk properties are uninsured - making the South the region with the largest number of potentially uninsured properties with significant flood risk.

The ABC OTV analysis shows some large coastal metropolitan areas also have double-digit rates of properties with significant flood risks, but lower rates of property owners with flood insurance.

In the storm-prone Houston, TX metro area (Austin, Brazoria, Chambers, Fort Bend, Galveston, Harris, Liberty, Montgomery and Waller counties), data show that 35% of 2.5 million properties are at major or above risk for flooding by 2053, but only 20% of all properties are covered by FEMA flood insurance policies.

In San Francisco, CA's metro counties -- Alameda, Contra Costa, Marin, Napa, San Francisco, San Mateo, Santa Clara, Solano and Sonoma - an estimated 16% of 2.1 million properties are at major or above risk for future flooding, while only about 2% of those properties have FEMA flood insurance.

The ABC OTV analysis findings and researchers perspectives about uninsured homeowners in substantial flood risk areas reflect many of those in a 2022 national survey conducted by the Federal National Mortgage Association (Fannie Mae).

The Fannie Mae survey was designed to help emergency management officials better understand homeowners' awareness and attitudes about flood insurance.

The survey included 3,500 homeowners with properties in FEMA's high and medium-risk flood zones, and adjacent areas.

Among the overall Fannie Mae survey findings:

The survey also found racial disparities in homeowners' awareness of flood risks and insurance programs.

Only 26% of non-Whites surveyed were aware they lived in high-risk flood zones, compared to 40% of White respondents.

In high-risk flood areas, about 46% of non-White homeowners were aware of FEMA flood insurance, compared to 56% of White homeowners.

Non-White homeowners in high-risk areas were less likely to have been told about flood risk before buying their homes than White homeowners. Only 35% of non-White homeowners were told about flood risk, compared to 44% of White homeowners, according the survey.

Contributing: Associate Producer Jared Kofsky, ABC-TV News, NY

Page development: Grace Manthey | Data analysis and reporting: John Kelly, Mark Nichols, Grace Manthey, Frank Esposito, Lindsey Feingold, Maggie Green, Maia Rosenfeld | Visual content producer: Adriana Aguilar | Video producers: Justin Allen, Christopher Drew | Digital production: Rachel Schwartz, Alex Meier, Margeaux Jimenez, Kristen Hague

Ⓒ 2023 ABC Owned Television Stations